Brought to you by Wealth Manager

The hunt for ethical riches

ESG

sponsors

contents

Listen

Watch

Read

The exciting new US frontier

podcast

Will Biden be a gamechanger for US ESG?

poll

Earn one hour of structured CPD

structured cpd

Vote

Content from: Fidelity

Sustainability is key for value creation

Images credit: Unsplash, Istock, Getty Images and Adobe Stock

How to avoid ESG disasters

FILM: the Art of Engagement

Fishing for the perfect allocation

Active vs passive, or both

Serious about sustainability

Content from: Natixis

With ESG now hardwired into the investment psyche, we explore how to build a sustainable portfolio based on the most important investment theme in history

Buyers’ favourite funds

UNDERCOVER SELECTOR

UK equities are shining brighter for responsible and sustainable investors

Content from: Edentree

How BMO lead the way in ESG engagement

Content from: BMO

by John Schaffer

Fund managers are faced with the perennial challenge of investing in profitable companies, while being ethical. However, sometimes ESG managers do get it wrong. One example of a problem company widely featured in ESG-focused funds was fashion retailer Boohoo, which faced serious allegations about systematic wage abuses in its supply chain last year after an undercover sting. More recently several large fund groups shunned Deliveroo’s recent IPO, partially due to concerns over the firm’s working practices. These are high profile examples of the potential minefields fund managers face and why engagement is essential, not only to avoid them, but to push companies to behave better.

Allianz Global Investors Aegon Asset Management

Sponsored content

Film: Inflation Storm Podcast Undercover Fund Selector Film: The $16tn Question Poll Badly Behaving Bonds Desperately Seeking Income Structured CPD

editorial content

ESG funds have exploded in popularity over the last three years, with the trend accelerated by the pandemic. But which strategies are grabbing the smart money? A look at the strategies held in funds of funds, mixed asset vehicles and model portfolios in Citywire’s exclusive data which hold a Morningstar ESG label suggests a relatively small group of mandates are favoured by institutional investors. Of the top 10 most widely-held products, five are held by at least 10 firms. All of the 10 top names attracted inflows of more than £100m in the year to the end of March, but some of the most widely-held strategies are in a league of their own. For example, The Royal London Sustainable Leaders trust – held in at least 24 portfolios by 10 firms – pulled in £1.28bn, while the Ninety One Global Environment fund took in £829m. Another fund deserving of mention here is Rathbone’s Ethical Bond fund, which also came top in our first Forecast’s roundup of most popular fixed income funds. It saw £955m in inflows. The below chart shows how many vehicles hold each of the 10 most widely-held ESG funds, along with a toggle to show the minimum number of asset management and wealth management firms that own them. By scrolling over the boxes you can also see which firm or firms hold each fund in the most portfolios.

When selecting funds for our models, their role in a holistic portfolio is what is pivotal to us. We do not select funds in isolation. With that in mind, three funds, Liontrust Sustainable Future UK Growth, Royal London Sustainable Leaders trust and Rathbone Ethical Bond fund each have a role among our other holdings. The Liontrust fund is more mid-cap and ‘growth’ focused. Royal London is larger cap and more core. Both are officially UK based. However, along with the larger cap exposure, Royal London carries more exposure to non-UK earnings. The US dollar exposure from Royal London serves a number of purposes. The dollar is often a currency of choice in risk-off panics, such as Brexit and Covid, and the US is still low on decent ethical or socially responsible funds. The Royal London Sustainable Leaders fund helps. However, when risk-on evolves, and with it the pound, Liontrust Sustainable Futures UK growth can thrive. On the bond side, Rathbones Ethical bond carries some equity correlation, with a fair exposure to BBB rated bonds, at 68.75% of assets, and a portfolio duration of over seven years, giving some rates exposure away from gilts. However, as these bonds are backed by businesses with a more sustainable, longer term mentality, we garner some comfort that management is perhaps more risk averse than a non-ethical peer group, more likely to survive and keep paying us relatively strong (to banks and gilts) levels of income.

Barry Cowen, fund manager at Sanlam Wealth

We are confident in the ability of WHEB Sustainable's team to deliver alpha over the long term through its small and mid-cap biased, quality growth, low turnover approach to sustainable investing. The fund is designed to benefit from companies providing solutions to environmental and social challenges that the world faces. These challenges provide multi-year growth opportunities which we believe the fund should benefit from over time. As sustainability challenges deepen and become more apparent, the benefits to the fund should increase. It is likely we will see a series of more meaningful policy decisions supporting the shift to sustainability over the next few years and this should benefit the portfolio. We believe this is an excellent way to gain exposure to genuinely sustainable businesses that are having a positive impact on society with meaningful growth potential.

Katie Trowsdale, head of multi manager strategies at Aberdeen Standard Investments

by Robin Amos

Liontrust Sustainable Future UK Growth

Royal London Sustainable Leaders Trust

FP Foresight Global Real Infras

Janus Henderson Global Sustainable

Sarasin Responsible Corporate

Threadneedle UK Social Bond

Liontrust Sustainable Future Corp Bond

FP WHEB Sustainability

Ninety One Global Environment

Rathbone Ethical Bond

Sanlam (4)

Casterbridge Wealth (6)

Sanlam (5)

Liontrust (5)

Casterbridge Wealth (3)

Canaccord Genuity (3) Brooks Macdonald (3)

EQ Investors (2) Kingswood (2) Cazenove Capital Schroder & Co (2)

VEHICLE

FIRM

Most held ESG funds

Hawksmoor Investment Management (3)

BMO Edentree Fidelity Natixis

Film: The Art of Engagement Undercover Fund Selector Podcast Poll Fishing for the perfect allocation Structured CPD

Click to download the chart

The value of investments and any income from them can go down as well as up and investors may not get back the original amount invested. Past performance should not be seen as an indication of future performance. All fund performance data is net of management fees. Screening out sectors or companies may result in less diversification and hence more volatility in investment values. The information provided in the marketing material does not constitute, and should not be construed as, investment advice or a recommendation to buy, sell or otherwise transact in the Funds.

Our heritage spans back to the launch of Europe’s first ethically screened fund in 1984 and a host of product launches and initiatives in the years since. We’ve been engaging companies on ESG matters for more than two decades, during which time we’ve had conversations with 5,500+ businesses in 87+ countries, resulting in over 4,000 instances of positive change in business practices. In 2005, we were one of the 100 founder signatories of the UN Principles for Responsible Investment; more recently, we became a founder signatory of the Net Zero Asset Managers Initiative, with an ambition of reaching net zero emissions by 2050 or sooner across all assets under management.

the BMO responsible investment team’

We believe that active ownership is key. Why? Because we don’t assume that our responsibility ends when an investment is made.

Source: Bloomberg

Source: Morningstar Direct. Manager Research. Data as of December 2020.

Our capabilities are always developing and evolving. Today, our Responsible Investment team comprises over 20 sustainability experts with skills spanning ESG analysis, engagement, screening and proxy voting. The team’s remit is a broad one, and their expertise ranges from corporate governance and labour standards to climate change, environmental stewardship and business conduct. In addition, we’re able to draw on the expertise of our Advisory Council, which comprises external experts who provide valuable perspectives on related issues. If we take climate change as an example, here are some of the ways in which our capabilities and approach have developed: • We’ve mentioned becoming a founder signatory of the UN PRI in 2005 and 15 years later the Net Zero Asset Owners Alliance. • From an active ownership perspective, we began engaging on climate change in 2000 as a founding theme for our reo® service, started systematically asking companies for climate scenario analysis in 2014 and integrated climate change into voting policies in 2019. • In terms of ESG integration, in 2012 we began producing ESG portfolio analytics that included carbon footprint analysis, and in 2016, we published our first impact report that included climate metrics. • 2011 saw the launch of the Climate Opportunity Partners Private Equity Fund, and in 2017 we committed to zero fossil fuel reserves across our responsible funds. • In 2019, we launched our BMO SDG Engagement Global Equity Fund, in which we engage extensively with companies around SDG 13: Climate Action.

We believe that active ownership is key. Why? Because we don’t assume that our responsibility ends when an investment is made. There is a sound rationale for this standpoint: we believe that through engagement, we can drive positive change in how companies operate from an ESG perspective, which in turn serves to reduce risk and enhance long-term performance potential. The importance of active ownership is increasingly recognised, but having the right skills and position from which to drive impactful dialogue with companies is key. Our Responsible Engagement Overlay (reo®) service offers third parties access to our full suite of stewardship expertise, including research, screening, engagement and proxy voting. Currently, our reo® service encompasses over £272bn in assets under advice, with our stewardship activities creating one single, powerful voice for positive change.

How have you developed and honed your responsible investment capabilities over the years?

Being responsible about investment sits at the core of our business and there are several elements to our related activities. Firstly, the breadth and depth of expertise facilitates our ambition of being a thought leader as we seek to share actionable insights with our clients and beyond. The team’s thinking is made available through our ESG Viewpoints and Pioneer Perspectives, which are all available on our website. Secondly, we are active owners seeking to bring about positive change by exerting our influence through thoughtful engagement with companies and by exercising voting rights. Thirdly, we work to ensure that ESG considerations are integrated into our investment analysis, as this provides a more comprehensive and rounded risk perspective. And finally, we offer a comprehensive suite of responsible products – each one underpinned by our defined Avoid, Invest, Improve philosophy.

What is your responsible investment philosophy?

How important is engagement to your investment process?

What is BMO’s heritage in responsible investing?

Responsible investment is becoming an increasingly ‘us too’ marketplace, so it’s key for clients to really consider whether an asset manager’s credentials are what they seem. We think our authenticity sets us apart. Our heritage is a long one and our capabilities are extensive and wide ranging. Perhaps our key differentiator, though, is how responsible considerations are integral to our entire ethos as a business. We’re not an asset manager that just happens to offer some ESG-orientated funds alongside our other products – being responsible about investment sits central to all our activities and processes.

In an increasingly crowded space, what sets BMO apart?

Responsible investment has moved mainstream and the role our industry must play in helping the world respond to major global challenges such as climate change is well recognised. We think this is a great move forwards and are committed to continuing to pioneer action in this space. For our business more specifically, we will continue to expand and refine our related product offerings. There’s scope to add more alternative options to our line-up, expand thematic orientated funds across asset classes and position ourselves as a one-stop-shop for ESG investing.

What’s next for you and the wider ESG universe?

CONTENT BY

For more information on Responsible Investing at BMO and our award-winning ranges, please contact sales.support@bmogam.com or visit bmogam.com/responsibleinvesting

The value of an investment and the income from it can fall as well as rise as a result of market and currency fluctuations, you may not get back the amount originally invested. Past performance should not be seen as a guide to future performance. If you are unsure which investment is most suited for you, the advice of a qualified financial adviser should be sought. EdenTree Investment Management Limited (EdenTree) Reg. No. 2519319. Registered in England at Benefact House, 2000, Pioneer Avenue, Gloucester Business Park, Brockworth, Gloucester, GL3 4AW, United Kingdom. EdenTree is authorised and regulated by the Financial Conduct Authority and is a member of the Investment Association. Firm Reference Number 527473.

The UK has one of the longest standing histories in respect of responsible and sustainable investing, and the region has been a fruitful source of returns for ESG investors over the long term. The last few years, however, have been difficult for responsible and sustainable investors in UK equities. A combination of negative Brexit sentiment and the coronavirus pandemic have weighed heavily on share prices and hampered investor confidence in the market. Although demand for ESG investing continues to grow more widely, the UK has been largely overlooked and under-allocated to, as other regions have outperformed. Despite this, at EdenTree we remain committed responsible and sustainable investors in UK equities. We believe the UK has a unique opportunity to take a global leadership position as a market for ESG investors, driven by a number of sustained industry trends and a more supportive macro-economic picture for UK equities as we move through 2021.

from Ketan Patel & Philip Harris

Rich seam of opportunities in UK ESG leaders

The pandemic has brought social issues into much greater prominence, clearly highlighting the social inequities and injustices that exist within the current global financial and economic system

A key development is the enormous shift in attitude towards ESG issues that we have seen over the last few years, putting the UK government and capital markets on a positive trajectory to embrace responsible and sustainable factors. For example, we now have previously unseen commitments from the UK government to achieving environmental targets. The pandemic has accelerated this trend in a number of ways. Firstly, it has brought social issues into much greater prominence, clearly highlighting the social inequities and injustice that exist within the current global financial and economic system. Secondly, the vast wave of new fiscal stimulus packages to combat the pandemic slowdown in most major developed economies is noticeably targeting green technologies and infrastructure. This was apparent in the UK’s stimulus package, which included plans to quadruple offshore wind power, boost hydrogen production, invest in carbon capture technologies and make London the capital of green finance. Finally, we are seeing strong support from financial institutions and industry bodies to make positive change. For example, Andrew Bailey, the governor of the Bank of England, has spoken out on the important role that capital markets have to play in achieving the transition to a resilient, carbon-neutral economy. This, combined with the supportive macro-economic backdrop – low interest rates and low inflation driven by ongoing monetary and fiscal policy – and hopes of the UK economy re-opening as the vaccine rollout continues, is leading us on an irreversible trend towards an increased responsible and sustainable opportunity set for UK equity investors.

Responsible and sustainable investors in UK equities are now faced with a potentially compelling investment opportunity, provided they are willing to look through the noise and short-term uncertainty. ESG investors must focus on how the UK is positioned for longer-term future growth, combined with the fact that the region provides a rich seam of companies that are ESG leaders, across sectors such as healthcare, industrials, materials and technology, providing us as responsible and sustainable investors with plenty of stock-picking opportunities.

Supportive environment for ESG investors

This being the case, fund buyers who want to capitalise on this need an investment manager with a deep expertise of both the UK and the responsible and sustainable investment landscape. EdenTree brought one of the first ethical UK equity funds to market more than 33 years ago, so we are firmly embedded in the fabric of responsible and sustainable investing within the UK. EdenTree’s Responsible & Sustainable UK Equity fund and our Responsible & Sustainable UK Equity Opportunities fund provide investors with a more complete allocation to UK equities as a whole, which should deliver regardless of market environment. At the heart of our approach we are responsible and sustainable, bottom-up stock-pickers who look for quality growth and earnings quality across all the companies we invest in. This ‘quality’ is attributed to companies that are market leaders in their field with defendable market share, attractive profit margins and solid cash flows – growth and returns on capital can only be predicated on these key attributes. The EdenTree Responsible & Sustainable UK Equity fund focuses on investing in companies that are resilient across all types of economic climate, and exhibit strong fundamentals. Looking for these opportunities primarily across the large and mid-cap spectrum, such an approach has proven over the long term to result in significant outperformance and offer more protection through challenging market conditions. The EdenTree Responsible & Sustainable UK Equity Opportunities fund puts growth at the heart of its strategy. The team takes a highly analytical and hands-on approach to stock-picking, aimed at reducing risk and enhancing returns. Key to outperformance and adding alpha is the fund’s focus on the mid and small-cap space. Both funds are also managed in accordance with our responsible and sustainable approach. We fully integrate ESG risk factors across our investment process in order to deliver superior returns and add value for clients. This integrated approach covers four key areas: screening, engagement, governance and thought leadership research, for a truly active responsible and sustainable approach.

EdenTree’s Responsible & sustainable approach

Stars aligning for ESG investors in UK equities

UK equities overlooked

Ketan Patel, fund manager of the EdenTree Responsible & Sustainable UK Equity Fund

Philip Harris, fund manager of the EdenTree Responsible & Sustainable UK Equity Opportunities Fund.

When it comes to ESG investing, the US is still far behind Europe, but things may be starting to change. Morningstar’s head of sustainability research Jon Hale believes younger investors’ attitudes, coupled with the Biden administration, will redefine ESG in the world’s biggest economy.

by Loukia Gyftopoulou

This information is for investment professionals only and should not be relied upon by private investors. The value of investments and the income from them can go down as well as up and clients may get back less than they invest. Past performance is not a guide to the future. Investors should note that the views expressed may no longer be current and may have already been acted upon. Changes in currency exchange rates may affect the value of an investment in overseas markets. Investments in emerging markets can be more volatile than other more developed markets. Reference to specific securities should not be interpreted as a recommendation to buy or sell these securities, but is included for the purposes of illustration only. The Fidelity Sustainable Asia Equity Fund has the potential of having high volatility either due to its composition or portfolio management techniques. It can also use financial derivative instruments for investment purposes, which may expose it to a higher degree of risk and can cause investments to experience larger than average price fluctuations. Please note that at least 70% of the portfolio invests in Asia ex-Japan stocks with strong sustainability characteristics - a minimum ESG rating of BB by MSCI. However, the portfolio managers will aim to achieve a higher threshold, targeting at least 70% of the portfolio invested in companies rated BBB and above by MSCI. If unrated by MSCI, rated C or above by Fidelity Sustainability Ratings. Our ratings score issuers on an A-E scale and trajectory forecast based on fundamental bottom-up research and materiality assessment using criteria specific to the industry of each company. A focus on securities of companies which maintain strong environmental, social and governance ("ESG") credentials may result in a return that at times compares unfavourably to similar products without such focus. No representation nor warranty is made with respect to the fairness, accuracy or completeness of such credentials. The status of a security's ESG credentials can change over time. This material was created by Fidelity International. It must not be reproduced or circulated to any other party without prior permission of Fidelity. Investments should be made on the basis of the current prospectus, which is available along with the Key Investor Information Document, current annual and semi-annual reports free of charge on request by calling 0800 368 1732. Fidelity only gives information on products and services and does not give investment advice to retail clients based on individual circumstances. Any comments or statements made are not necessarily those of Fidelity. All e-mails may be monitored. Issued by FIL Pensions Management, authorised and regulated by the Financial Conduct Authority and Financial Administration Services Limited, authorised and regulated by the Financial Conduct Authority. Fidelity International, the Fidelity International logo and F symbol are trademarks of FIL Limited. UKM0321/34008/SSO/NA

Investing strategies focused on environment, social and governance factors, better known as ESG strategies, often employ screening, exclusions, and integration among other tactics. But at their core, all these strategies are about investing in ‘sustainable’ businesses. While simplistic, achieving a long-term future for any business hinges on sustainability pervading all aspects of the company. To be clear: a company that ignores its environmental externalities, is unable to retain talent, or isn’t compliant with regulations won’t be able to sustain its operations into the future. Conversely, as numerous studies have shown, companies with higher sustainability characteristics deliver superior long-term value. Here we clarify the link between sustainability and value creation. There’s general agreement about why this link exists - a business which doesn’t pursue stakeholder value creation or ignores the E, S or G aspects is bound to stumble and destroy value, like a car with one or more wobbly wheels. Here, we aim to address the ‘how’ of assessing this via our valuation approaches.

Dhananjay Phadnis, Lead Portfolio Manager

from Dhananjay Phadnis, Lead Portfolio Manager and Flora Wang, Co- Portfolio Manager, Fidelity Sustainable Asia Equity Fund

Most investors can agree that environmental, social and governance (ESG) factors help determine a company’s prospects for long-term value creation. But how should we quantify the valuation impact of sustainable investing?

Avoiding value destruction through a ‘sustainability’ lens

A recent example is China’s peer-to-peer (P2P) lending industry, which saw rapid growth until a few years ago. By June 2018, estimated P2P outstanding loans topped 1 trillion renminbi ($155 billion). Before regulators stepped in, companies such as Yirendai, Paipaidai and Qudian were charging effective interest rates as high as 35-40%. Since then, regulatory intervention has helped lead to a dismantling of China’s P2P lending industry. Investors looking at the sector’s rapid rise through a sustainability lens might have been better able to sidestep some of the value destruction that ultimately ensued. Interest rates charged by some companies were clearly excessive and unsustainable. The story of Martin Shkreli’s Turing Pharma is another case of an unsustainable business model, whereby the firm in its bid to boost profits, put through massive price increases for life-saving medicines that then became unaffordable for patients. Value destruction can also come from running businesses with unsustainable debt structures such as General Electric, which was recently forced to undertake significant asset sales to pare down debt.

Valuation implications

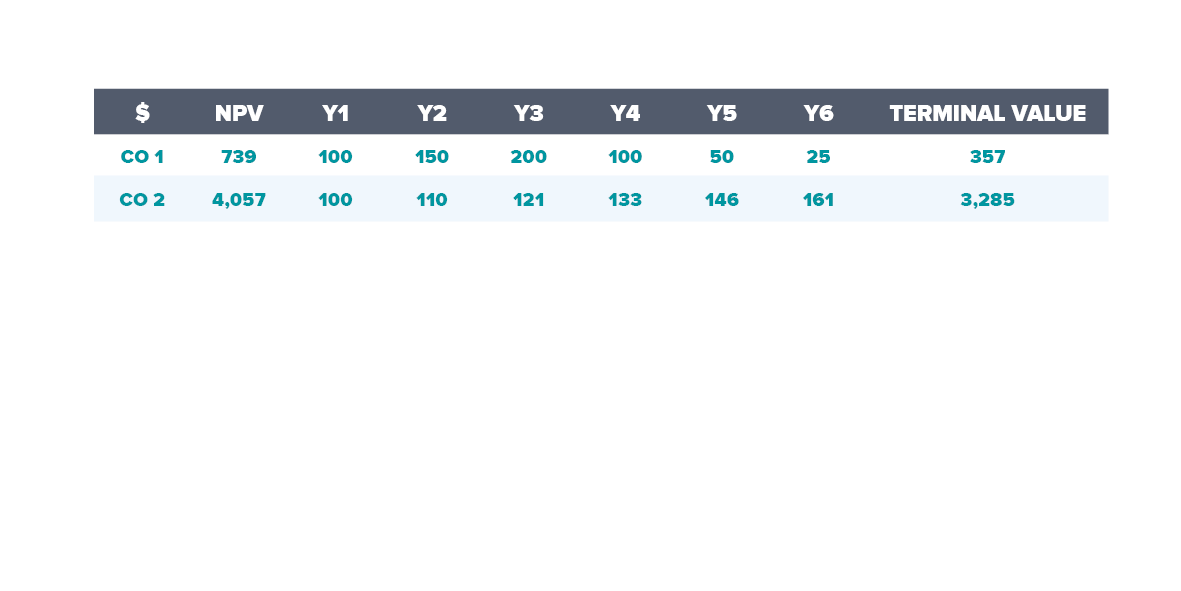

All valuation methodologies, whether traditional ones of price to earnings and price to book, or the recently popular ones like price to sales or enterprise value to sales, are essentially shortcuts to understanding the present value of future cash flows, which investors also calculate via a discounted cash flow (DCF) analysis. In the example below, Company 1 and Company 2 are in the same industry facing similar dynamics. They both generated $100 of free cash flow in Year 1. Company 1 focused on growth and has pushed a new generation product, despite potential safety hazards for its customers. Company 2 focused on product safety and was willing to invest in a higher R&D effort, at the cost of some near-term cash flows. After a few years, Company 1 experiences safety issues that triggers regulatory intervention, leading to a reset in its FCF down to $25 by Year 6. Additionally, there’s now no earnings growth potential for Company 1. Company 2 sees steady growth and gives us the confidence to project a 3% terminal growth for its products. Using a similar 7% discount rate for the two companies, we can see the results:

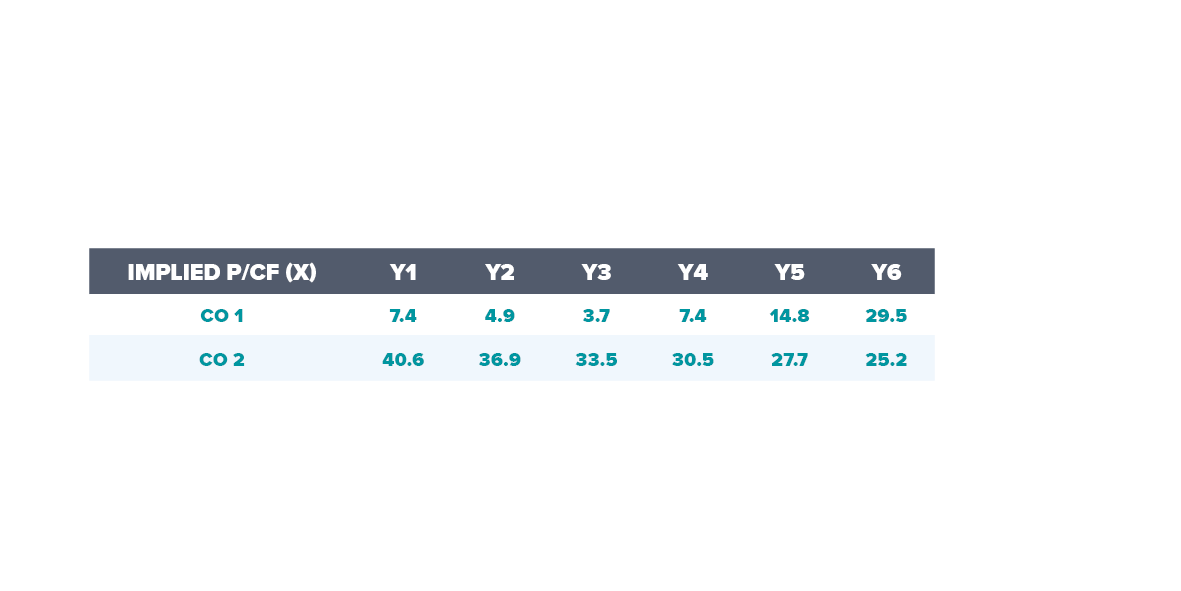

For simplicity, we discounted both companies by the same rate, but this might have been too generous. In reality, Company 1 should see its cash flows discounted by a much higher rate given the inherently higher risk in its business operations. As an alternate example, let’s take a look at another commonly used valuation metric - P/E ratios. This approach considers the earnings power of the business now and awards the company a ‘n’ number of years of realizing such earnings. While ‘n’ depends on a few other variables such as growth, returns and cost of capital, the sustainable period of excess returns is a key driver of the P/E multiple. When we look at P/E (we assume free cash flows are equivalent to earnings to keep it simple) for two companies in the early years of the forecast horizon, the results are stark. Company 1 deserved a much lower multiple to discount for the lack of sustainability in its operations. However, it is very likely that the market would ascribe it a much higher multiple than Company 2 in the early years of strong growth.

What are the red flags?

Some red flags to observe include excessive returns, complex business structures, lack of regulatory clarity, short-term focused management incentive structures, low or no focus on a stakeholder analysis, and reliance on debt to enhance returns. While not a comprehensive list, viewing any business through a sustainability lens can help investors allocate capital to companies that will drive long-term value creation and mitigate exposure to permanent loss of capital. In the case of the aforementioned Chinese P2P industry, excessive returns of the lenders, complex fee structures and lack of regulatory clarity were all red flags.

While simplistic, achieving a long-term future for any business hinges on sustainability pervading all aspects of the company

Source: Allianz Strategic Bond Fund C (Inc) GBP; Bloomberg, as at: 31/01/2021. Strategy inception date: 21/06/2016. Past performance is not a reliable indicator of future results.

That’s what makes sustainability important and key to long-term value creation. It can help close the gap between expectations and outcomes, while protecting an investment from a permanent loss of capital.

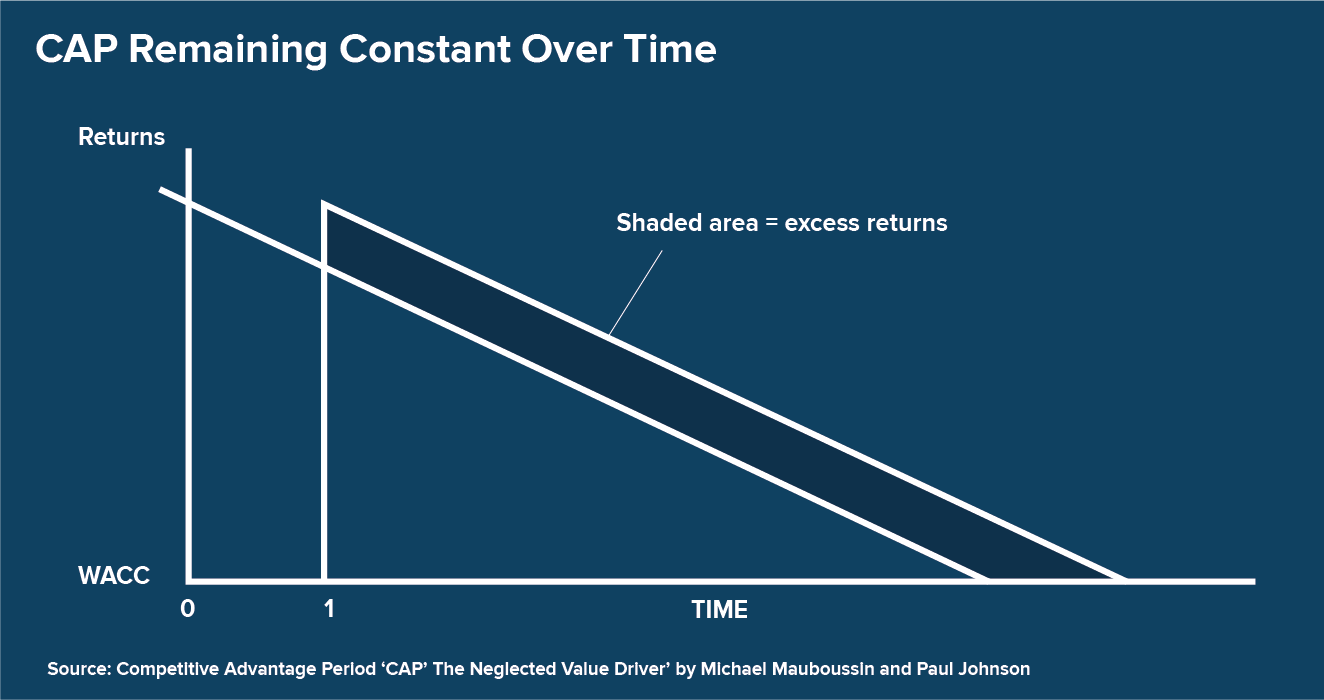

Sustainability of a business is a key input in estimating its potential for value creation. While analysts tend to focus on estimating the competitive advantage period, true sustainability comes when a business takes it farther, with a focus on relevant ESG aspects and by adopting a stakeholder-centric approach. A comprehensive evaluation of sustainability should be a key part of any investment analysis.

Register now: 11 May, 8:30-9:30am

The principle of sustainability is linked to the concept of Competitive Advantage Period (CAP) developed by Miller & Modigliani (1961), which was expanded upon by Michael Mauboussin and Paul Johnson (1997). Essentially, the longer a company can expand its CAP, the more value it creates. Let’s expand this concept further by calling it Sustainable Competitive Advantage Period (SCAP). This is a period during which, by virtue of its ESG and stakeholder-centric business practices, a company can reduce the risks to CAP longevity and prolong this period thereby driving value.

Inside Fidelity: Sustainable engagement

Learn about Fidelity’s active engagement

Learn more about the Fidelity Sustainable Asia Equity Fund

Sustainability - a key part of investment analysis

Flora Wang, Co-Portfolio Manager

Film: The Art of Engagement Undercover Selector Podcast Poll Fishing for the perfect allocation Structured CPD

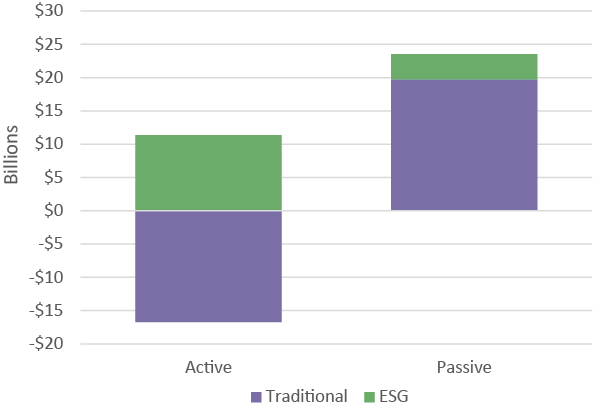

While the rise of passive investment funds has been one of the stories of the last decade, it has not always chimed with ESG investing. To emphasise how influential passive has become, this type of investing has attracted $24.5bn (£17.8bn) in the last two years. In comparison, active equity funds have seen $5.4bn in outflows, a figure which would have been 211% higher at $16.8bn if ESG strategies were not factored in.

by Theo Andrew

Active vs passive, or both?

A dual approach

Turning tides

For some, passive investing is simply not an option when considering ESG. While Hampton’s preference is active management, she concedes there is growing engagement on the passive side, but that it still varies widely by manager. ‘It is clearly a challenge to ensure a consistent, rigorous approach given the volume of holdings within passive products,’ she said. However, for others, it is still early days for the industry in terms of the quality of data standards among ratings agencies, and this is only going to improve. ‘There are considerable areas across a range of different topics which will only improve, consolidate and see innovation,’ Emery said. ‘That will continue throughout the next five to 10 years and onwards.’ Damien Lardoux, head of impact investing at EQ Investors, added that the innovation will come and that engagement within the industry is helping to spot gaps and areas of improvement. ‘There are products being launched every week so spaces are getting a bit crowded, but there's definitely some space where there's a lot of innovation that can be made.’ Over 2020, 31 dedicated socially responsible ETFs were launched, most notably BlackRock’s iShare ESG MSCI EM Leaders fund which drew in $800m (£582m). Lardoux believes one area to watch is green bonds, although he admits the pace of change could make it difficult for smaller firms to keep track. ‘The investment universe is growing very quickly. If you look at green bonds 10 years ago you had very few, but now you have corporate bonds in developed and developing markets,’ he said. ‘It is a space that is moving so quickly that it's actually quite hard to keep pace, it takes a lot of time to make sure you remain at the cutting edge of innovation.’

One approach that is growing in popularity is utilising passives as building blocks for a wider sustainable portfolio. This is a trend spotted by Invesco multi-asset fund manager Clive Emery, who oversees five low cost risk-targeted portfolios within the fund giant’s Summit Responsible Range, comprising baskets of ETFs. To overcome the engagement hurdle, Emery works closely with the firm’s active business. ‘Passive and active will both have an important role and I think passive is evolving its approach. It is developing its proxy voting and engagement as much as possible,‘ Emery explains. ‘We can use that approach to optimise that non-financial criteria and that level of clarity and transparency in the approach that passives can bring to bear.’ Hampton believes forward looking products aligned to legislation such as the Paris agreement, which has year-on-year decarbonisation targets, are encouraging. However, she leans towards an active approach in her portfolios. ‘We prefer active approaches where the thematic exposure can be considered as part of the overall business and where valuation rigour can protect against concentration in companies where valuations are overstretched,’ she said. Some of the best performing passive strategies over 2020 were heavily tilted towards a particular theme within ESG. For example Invesco’s Solar ETF and WilderHill Clean Energy ETF delivered returns of 223% and 196% respectively. While some active funds also saw impressive returns, they remained someway off. The Guinness Sustainable Energy fund, one of the top performing clean energy funds over 2020, returned 84.1%. On top of this, the passive returns were also achieved at a much lower price for investors. The Invesco Solar ETF achieved its performance with an annual management fee of 0.5% compared to an ongoing fund charge of 1.99% for the Guinness Sustainable Energy fund, but this could come at a cost according to Hampton. ‘The difficulty for investors is knowing which passive managers have this capability and are delivering on it and which aren’t,’ she said.

This boom in sustainable investing has proved to be an important differentiator for active managers in the competition with passive strategies, which has put them under intense pressure. One big advantage active has had over passive is the ability to engage in a transparent and effective way to influence companies’ ethical behaviour. Cazenove Capital sustainable investment director Catherine Hampton underlines how this works in practice. ‘Sustainable strategies also need the option to actively divest from holdings if they no longer meet the high bar for inclusion. For example, if engagement hasn’t been successful - this is not possible within passive approaches.’ However, the climate is changing and with constant improvements to data quality and the rise of proxy voting, alongside some decent performance, passive’s influence in ESG is starting to gain traction.

2019 - 2020 ESG V Traditional Equity

This material is provided for informational purposes only and should not be construed as investment advice. The views and opinions expressed are as of April, 2021 and may change based on market and other conditions. There can be no assurance that developments will transpire as forecasted, and actual results may vary. Before investing, consider the fund’s investment objectives, risks, charges, and expenses. You may obtain a prospectus or a summary prospectus on our website containing this and other information. Please read it carefully. This material is provided by Natixis Investment Managers UK Limited (the ‘Firm’) which is authorised and regulated by the UK Financial Conduct Authority (register no. 190258). Registered Office: Natixis Investment Managers UK Limited, One Carter Lane, London, EC4V 5ER. When permitted, the distribution of this material is intended to be made to persons as described below: In the United Kingdom: this material is intended to be communicated to and/or directed at investment professionals and professional investors only. In Ireland: this material is intended to be communicated to and/or directed at professional investors only. In Guernsey: this material is intended to be communicated to and/or directed at only financial services providers which hold a license from the Guernsey Financial Services Commission. In Jersey: this material is intended to be communicated to and/or directed at professional investors only. In the Isle of Man: this material is intended to be communicated to and/or directed at only financial services providers which hold a license from the Isle of Man Financial Services Authority or insurers authorised under section 8 of the Insurance Act 2008. To the extent that this material is issued by Natixis Investment Managers UK Limited, the fund, services or opinions referred to in this material are only available to the intended recipients and this material must not be relied nor acted upon by any other persons. This material is provided to the intended recipients for information purposes only. This material does not constitute an offer to the public. It is the responsibility of each investment service provider to ensure that the offering or sale of fund shares or third party investment services to its clients complies with the relevant national law. The above referenced entity is a business development unit of Natixis Investment Managers, the holding company of a diverse line-up of specialised investment management and distribution entities worldwide. The investment management and distribution subsidiaries of Natixis Investment Managers conduct any regulated activities only in and from the jurisdictions in which they are licensed or authorized. Their services and the products they manage are not available to all investors in all jurisdictions. Although Natixis Investment Managers believes the information provided in this material to be reliable, including that from third party sources, it does not guarantee the accuracy, adequacy, or completeness of such information. The provision of this material and/or reference to specific securities, sectors, or markets within this material does not constitute investment advice, or a recommendation or an offer to buy or to sell any security, or an offer of services. Investors should consider the investment objectives, risks and expenses of any investment carefully before investing. The analyses, opinions, and certain of the investment themes and processes referenced herein represent the views of the portfolio manager(s) as of the date indicated. These, as well as the portfolio holdings and characteristics shown, are subject to change. There can be no assurance that developments will transpire as may be forecasted in this material. This material may not be distributed, published, or reproduced, in whole or in part. Mirova is affiliate with Natixis Investment Managers. MIROVA Limited liability company RCS Paris no. 394 648 216 Regulated by AMF under no. GP 02-014 59 Avenue Pierre Mendès-France, 75013 Paris. Mirova US 888 Boylston Street, Boston, MA 02199; Mirova US is a U.S.- based investment advisor that is a, wholly owned affiliate of Mirova. Mirova is operated in the U.S. through Mirova US. Mirova US and Mirova entered into an agreement whereby Mirova provides Mirova US investment and research expertise, which Mirova US then combines with its own expertise when providing advice to clients

I was working for a Belgian bank, KBC, at the beginning of my career, which also had an asset management business. They hired me as a financial analyst. We were working together with an Irish team and, at the time, there were a number of common projects. Ultimately, KBC asked me to move to Dublin to further develop their thematic strategies from Dublin. Towards the end of the 90s there was a lot of talk about technology and the ‘next generation’. In contrast, there was also growing awareness of demographic changes in the developed world and KBC had launched a fund focused on investments related to an ageing population. In addition, there were also strategies related to water and alternative energy, as well as financial themes like IPOs and buybacks. Although the strategies proved very successful, a lot of the growth came through performance rather than inflows. I witnessed competitors emerge and raise millions and sometimes billions with a shorter or less compelling track record than ours. In the mid-2000s, I went with a business plan to my senior management at the time which effectively said, ‘Listen guys, if you’re serious about becoming a world leader in thematic investing, we need to build a dedicated team around that’. So we built out a thematic team which very quickly began to focus purely on the environmental side of those themes. We launched an agricultural strategy, as well as a climate change strategy and a multi-environmental strategy. Fast forward 10 years and, one day, I received a call from Philippe Zaouati (Global CEO of Mirova), who I had met on several occasions. He asked me whether I’d be interested in joining the new sustainability branch of Natixis, which a few months later was renamed Mirova. I accepted and moved to Paris.

Jens Peers CEO, CIO & Portfolio Manager Mirova US

By Jens Peers

‘We try to find companies that… are among the first movers within their peer group. Then we then try to identify the laggards. And finally we connect the dots. There's no magic formula to it, unfortunately.’ ‘Instead of being a satellite allocation, I felt that such an investment strategy could have its place in the core of an investor’s portfolio.’

For me, it was an opportunity to broaden out from pure environmental investing, especially given I had past experience managing demographic strategies as well. The way I saw it, there were so many opportunities to bring a range of themes together in a single portfolio fund. Instead of being a satellite allocation, I felt that such an investment strategy could have its place in the core of an investor’s portfolio. However, for this to work it would require the support of a large team of analysts and portfolio managers covering a wide range of areas beyond just environmental equities. This was exactly what Mirova had to offer in addition to the global reach of the Natixis organization as a whole.

As a company whose ‘raison d’etre’ is about creating a positive impact, we’ve been forced to ask ourselves whether the rise of more mainstream managers positioning themselves on the topic of ESG is a good or a bad thing. I think on the one hand it's positive because it helps raise awareness for companies like ours. Even though many of these companies may have much deeper marketing pockets than we might. But just like the water strategy I was managing back in the 2000s, at the time it probably would not have grown as much as it did if it wasn't for some big competitors spending a lot of euros bringing attention to water as an investment opportunity. That said, there’s a big risk of ‘greenwashing’, even though I very much dislike the term. It is important to make sure that people understand what the different degrees or different approaches are to ESG so that they can compare apples to apples. And that's something I feel is still missing in the market. Do we need to evolve our business model as a result? The way I see it, historically 5-10% of investors wanted to be more sustainable than the average. As the rest of the market begins to move in their direction, they may feel the need to become increasingly more extreme. For those clients we have a range of solutions, from Amazon rainforest preservation strategies, ocean clean-up strategies or land degradation strategies.

To learn more visit: www.im.natixis.com/uk/esg-sustainable-investing-solutions

It is likely that the composition of tomorrow's stock market indices will look very different than they do today. In the years to come, there’ll be less demand for fossil fuels, continued demographic change and ever more scrutiny of environmental, social and governance-related responsibilities. Companies will need to adapt their business models and practices if they are to stay competitive. And some are already making great strides in the right direction. Jens Peers, CEO & CIO of Mirova US and manager of the Mirova Global Sustainable Equity Strategy, reveals how nearly two decades of thematic and environmental investing have helped hone his skills in identifying the companies that are transitioning towards the future.

What interested you about Mirova?

We do a lot of research. We talk to people, we talk to companies. We make sure we're surrounded by good people in our own company as well. We're one of the few houses to have a dedicated ESG team that’s been together for so long. What we’re looking for is the speed at which various companies are transitioning their businesses toward the future. We see a world where the demand for fossil fuels will be in decline. It’s a world undergoing continued demographic change, be it population growth or urbanisation. And it’s a world where corporate governance and corporate social responsibility come under increased scrutiny. We try to find companies that have identified trends such as these early, and that are among the first movers within their peer group. Then we then try to identify the laggards. And finally we connect the dots. There's no magic formula to it, unfortunately.

You launched Mirova’s Global Sustainable Equity Strategy in 2013. How do you go about identifying suitable investment candidates for the strategy?

Can you provide examples of companies that have been successful at doing this in the past?

You’re the CEO of Mirova US and living in Boston. Where did it all start for you?