Brought to you by New Model Adviser

Discover four of the most important challenges for ESG investors

Fire, Water, Earth, and Air

Digging for battery parts has a carbon cost

ESG

sponsors

contents

Listen

Watch

Read

Earth

Content from: FIDELITY

Sustainability is key for value creation

Why wildfires are a burning issue

podcast

How many clients are in sustainability-focused funds?

poll

The funds piling into wind power

AIR

Vote

Clean water from dirty power? Not if investors have their way

WATER

Content from: EDENTREE

Rich seam of opportunities in UK ESG leaders

Content from: BMO

At the heart of responsible investing

Images credit: Unsplash and Istock

Structured CPD

Earn one hour of structured CPD, endorsed by the CII

EARTH

Driving is a drug that is hard to kick. According to NatCen’s 2019 UK National Travel Survey, 61% of all trips that year were by car. Every journey adds up to those big carbon numbers. More than a third of Europe’s CO2 output is due to transport emissions, and road transport accounts for 71% of that. Air pollution has many silent health effects that include stunting the development of children’s lungs as well as respiratory and cardiovascular diseases in older people. Adding the cost of health problems to other economic impacts of dirty air – which has been shown to deter both tourists and workers – the World Bank and Institute for Health Metrics and Evaluation have claimed the global cost of air pollution could be as high as $225bn (£164bn). Perhaps this is why in January the market capitalisation of electric car manufacturer Tesla dwarfed that of Big Oil, reaching $834bn compared with ExxonMobil’s $192bn. But electric cars are not as green as they seem.

By Will Robins, Editor

Digging for battery parts is dirtier than it seems

Rare earth

One question to be asked about the carbon footprint of electric vehicles is how the electricity used to charge them is made. If it is by burning fossil fuels, the benefit of battery power might be marginal, or localised to places suffering from high levels of exhaust pollution. But there is another issue for the ESG investor too – how the batteries are made. It is here that talk of rare earth begins. Rare earth is a catch-all term for the metals used to manufacture batteries, including the one in your smartphone. Lithium is one of these rare-earth metals. As the name suggests, these metals are hard to get to. The issue is not so much that there are not enough of the elements in the ground, but that they are distributed sparsely. That requires a lot of digging, which in turn burns fossil fuels. All the emissions resulting from the manufacture of a lithium-ion battery are referred to as ‘embedded’. Since the production of a battery requires around 20 different materials, all of which need refining and transporting, the value chain is long and complex. According to a 2019 research paper on the climate impact of lithium-ion batteries published by Circular Energy Research and Consulting:

Half a million gallons of water are used to produce each tonne of lithium. In some parts of South America, mining activities take up about 65% of the region’s water supply.

Does this mean EVs are – excuse the pun – non-starters? That depends on whether batteries tip the scales away from fossil fuels in the overall energy system. If batteries last longer when used and store electricity for longer when not being used; if they can be reused; if they can give electricity back to the grid when parked; or if batteries are used to store electricity from a wind turbine or solar cell, then massive efficiency can be unlocked. Storing power in batteries so that it can be called upon at moments of peak demand means power stations are not having to ramp up production themselves. It may seem anachronistic in today’s world of streaming, but a phenomenon known as TV pickup used to give National Grid a real headache. When a large number of people watch the same TV show at the same time, their use of electrical appliances – nipping to the kitchen to put the kettle on during an advert break – is synchronised too. Soaps and must-see dramas were the most common causes, but the biggest were sporting events, and none more so than football. The 2018 football World Cup game between England and Colombia generated a 1,200 megawatt (MW) demand at half time. But the record was set in 1990, during the World Cup semi-final match between England and West Germany. According to Drax.com, demand hit 2,800MW, which is equivalent to the boiling of more than one million kettles. Talk about tea and sympathy! As battery investor Gresham House explains: ‘Without the ability to store renewable energy, it is difficult to balance supply and demand effectively, meaning excess wind and solar generation produced at off-peak times of the day is wasted.’

Energy storage

To save the planet, we need to change the way we move. Stopping cars from blowing toxic emissions out of their exhausts seems a good place to start, but electric cars might come with complications.

Gresham estimates that instances of ‘temporary excess generation’ amounting to 10 gigawatts (1000MW) of wasted energy could occur frequently over the next four years. As renewables continue to replace more expensive – and dirtier – fossil-fuel power stations, this volatility will increase. Large lithium-ion battery systems allow energy to be stored for periods of higher demand, or when renewable supply is low. The ability to hold on to electricity creates an opportunity to buy energy cheaply and sell it back to the market at a higher price. Gresham House’s Energy Storage Fund investment trust owns 11 sites throughout the UK, representing a total 187MW of capacity, according to projections from its 2019 annual report. It represents a comparatively small change right now, but investors are hoping to capture a healthy return and steady income from being part of an infrastructure growth story. ESG investors will be heartened to know that producers of rare earths are under pressure to clean up the process of making it. The Initiative for Responsible Mining Assurance (IRMA) offers a certification process covering environmental impacts such as water use, waste management and greenhouse gas emissions, as well as social impacts such as fair labour terms and worker safety. Last year Mercedes-Benz announced it would only use batteries that sourced lithium and cobalt from IRMA-certified producers. Earlier this year, Ford became the first US automaker to become a member of the IRMA. South America’s Lithium Triangle, which is spread across Argentina, Chile and Bolivia, is home to 53% of the world’s lithium deposits. These reserves are located under dry salt flats that are drilled, pumping mineral-rich saltwater onto the surface. This evaporates on the surface for months, resulting in a mixture of salts, from which lithium carbonate can be extracted. Half a million gallons of water are used to produce each tonne of lithium. In some parts of South America mining activities take up about 65% of the region’s water supply. According to an S&P Global report, Chilean producer SQM announced its own IRMA certification process that will cut its use of brine by 50% by 2030 and cut its use of water by 40% and achieve carbon neutrality by 2040. The ability to capture and store renewable energy is vital to make the switch from petrol to electric vehicles environmentally worthwhile. That means using batteries in two different places – as part of the grid and in cars. This would suggest massive demand for rare-earth elements. Although the lithium-ion battery has played a crucial role in our move away from fossil fuels, the environmental cost of its production will outweigh its benefits in the long term. Companies will need to prove they are not doing more harm than good to convince investors, while laggard producers could end up penalised by more ESG-conscious and customer-facing companies such as Mercedez and Ford.

For funds investing in rare earths, check out Citywire’s Natural Resources sector. It lists 25 managers with more than 36 months’ track record.

‘If an electric vehicle is using a 40kWh (kilowatt-hour) battery, its embedded emissions from manufacturing would then be equivalent to the CO2 emissions caused by driving a diesel car, with a fuel consumption of 5 litres per 100km, in between 11,800km and 89,400km before the electric car even has driven one meter. While the lower range might not be significant, the latter would mean an electric car would have a positive climate impact first after seven years for the European average driver.’

BMO Edentree Fidelity Natixis

Sponsored content

Film: The Art of Engagement Undercover Selector Podcast Poll Fishing for the perfect allocation Structured CPD

editorial content

Fire

There has been a growing number of wildfires around the world in the last few years. As well as major fires in Australia and California, we have started to see more fires across Europe. A recent University of Reading report found there was an increased risk of wildfires in the UK. There have even been fires in the Arctic. We are joined by Guillermo Rein, professor of fire science at the department of mechanical engineering of Imperial College London, to discuss how companies can counter fire risk and how investors can help.

by Charles Walmsley, Investment editor

BMO Edentree Fidelity

Earth Fire Poll Air Water CPD Quiz

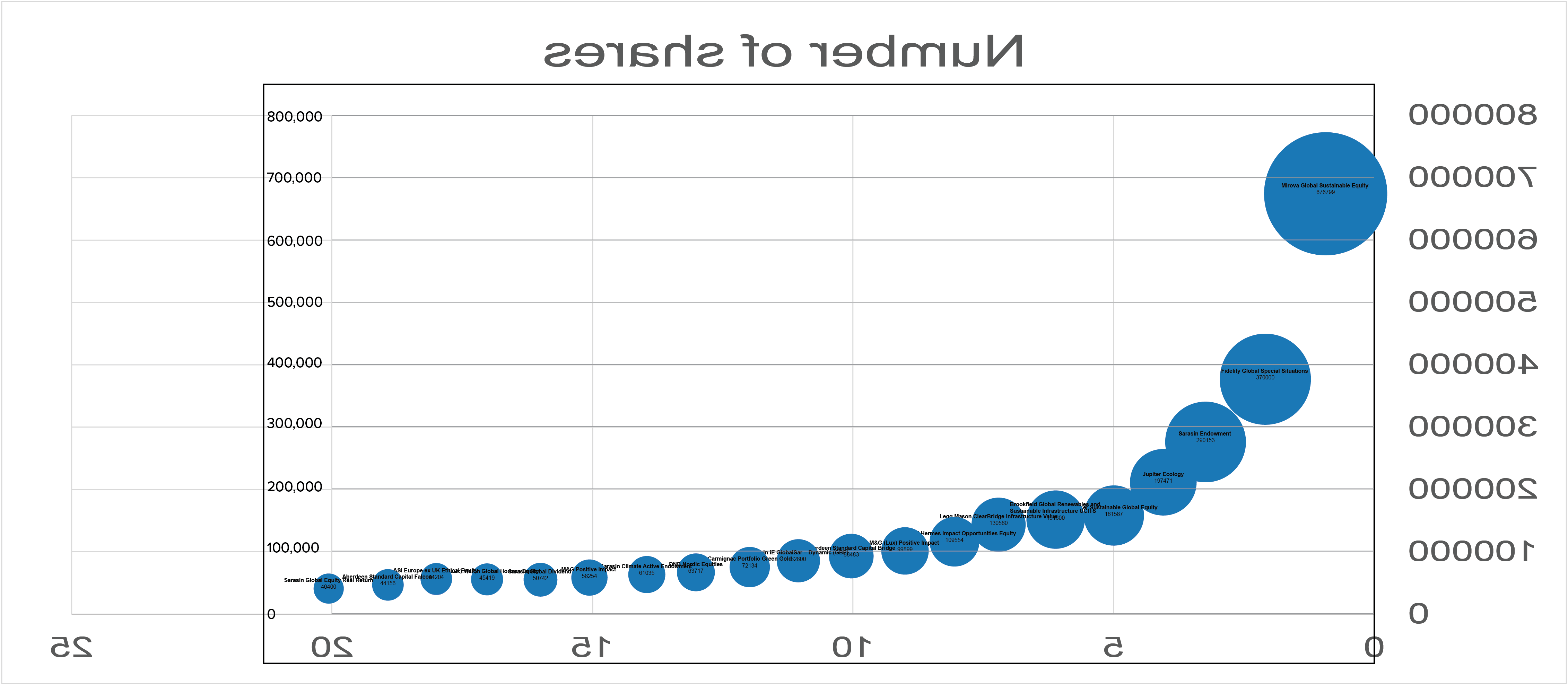

TOP 20 FUNDS HOLDING ØRSTED

Danish renewable energy provider Ørsted is best known for its wind farms. It set up the first onshore wind farm in 1991 and has a target of doubling its offshore wind capacity by 2025. That would mean using wind power to meet the electricity consumption needs of 30 million people, according to Ørsted. Last year wind generated DKK 40bn in revenues, so it is easy to see why the company has become a darling of ESG funds. Some might argue it has become too easy a choice for funds late to the sustainability game.

The ESG darling blowing investors away

Mirova Global Sustainable Equity

Number of shares: 676,799 First purchased: 2019 Weighting: 4.6%

Fidelity Global Special Situations

Number of shares: 370,000 First purchased: 2016 Weighting: 1.7%

Sarasin Endowment

Number of shares: 290,153 First purchased: 2018 Weighting: 2.1%

Jupiter Ecology

Number of shares: 197,471 First purchased: 2016 Weighting: 4.2%

Mercer Sustainable Global Equity

Number of shares: 161,587 First purchased: 2019 Weighting: 1.6%

Brookfield Global Renewables and Sustainable Infrastructure UCITS

Number of shares: 151,600 First purchased: 2020 Weighting: 6.7%

Legg Mason ClearBridge Infrastructure Value

Number of shares: 130,560 First purchased: 2020 Weighting: 3.5%

Federated Hermes Impact Opportunities Equity

Number of shares: 109,554 First purchased: 2018 Weighting: 4.8%

M&G (Lux) Positive Impact

Number of shares: 99,899 First purchased: 2018 Weighting: 5.4%

Aberdeen Standard Capital Bridge

Number of shares: 88,483 First purchased: 2019 Weighting: 2.3%

Carmignac Portfolio Green Gold

Number of shares: 72,134 First purchased: 2019 Weighting: 3%

DNB Nordic Equities

Number of shares: 63,717 First purchased: 2020 Weighting: 7%

Sarasin Climate Active Endowment

Number of shares: 61,035 First purchased: 2018 Weighting: 1.9%

M&G Positive Impact

Number of shares: 58,254 First purchased: 2018 Weighting: 5.4%

Sarasin Global Dividend

Number of shares: 50,742 First purchased: 2018 Weighting: 2.8%

RBC (Lux) Vision Global Horizon Equity

Number of shares: 45,419 First purchased: 2018 Weighting: 4%

ASI Europe ex UK Ethical Equity

Number of shares: 44,204 First purchased: 2018 Weighting: 2.4%

Aberdeen Standard Capital Falcon

Number of shares: 44,156 First purchased: 2019 Weighting: 2.5%

Sarasin IE GlobalSar – Dynamic (GBP)

Number of shares: 82,800 First purchased: 2018 Weighting: 1.9%

Sarasin Global Equity Real Return

Number of shares: 40,400 First purchased: 2018 Weighting: 2.4%

By James Fitzgerald, Reporter

The world’s clean water supply is running out. Climate change is pushing global populations towards urbanisation due to longer droughts and desertification. Revolutionary clean water solutions are needed to keep the tap running because much of the technology we use to extract and purify water is outdated, expensive or powered by fossil fuels. Sounds hopeless? Perhaps not. New Model Adviser reporter James Fitzgerald discovers that private investors are demanding clean water companies clean up their act, or face a drought of a different kind.

Our heritage spans back to the launch of Europe’s first ethically screened fund in 1984 and a host of product launches and initiatives in the years since. We’ve been engaging companies on ESG matters for more than two decades, during which time we’ve had conversations with 5,500+ businesses in 87+ countries, resulting in over 4,000 instances of positive change in business practices. In 2005, we were one of the 100 founder signatories of the UN Principles for Responsible Investment; more recently, we became a founder signatory of the Net Zero Asset Managers Initiative, with an ambition of reaching net zero emissions by 2050 or sooner across all assets under management.

by the BMO responsible investment team

What is BMO’s heritage in responsible investing?

How have you developed and honed your responsible investment capabilities over the years?

Our capabilities are always developing and evolving. Today, our Responsible Investment team comprises over 20 sustainability experts with skills spanning ESG analysis, engagement, screening and proxy voting. The team’s remit is a broad one, and their expertise ranges from corporate governance and labour standards to climate change, environmental stewardship and business conduct. In addition, we’re able to draw on the expertise of our Advisory Council, which comprises external experts who provide valuable perspectives on related issues. If we take climate change as an example, here are some of the ways in which our capabilities and approach have developed:

What is your responsible investment philosophy?

Being responsible about investment sits at the core of our business and there are several elements to our related activities. Firstly, the breadth and depth of expertise facilitates our ambition of being a thought leader as we seek to share actionable insights with our clients and beyond. The team’s thinking is made available through our ESG Viewpoints and Pioneer Perspectives, which are all available on our website. Secondly, we are active owners seeking to bring about positive change by exerting our influence through thoughtful engagement with companies and by exercising voting rights. Thirdly, we work to ensure that ESG considerations are integrated into our investment analysis, as this provides a more comprehensive and rounded risk perspective. And finally, we offer a comprehensive suite of responsible products – each one underpinned by our defined Avoid, Invest, Improve philosophy.

Name name is a job title job title at company

Risk disclaimer: The value of investments and any income from them can go down as well as up and investors may not get back the original amount invested. Past performance should not be seen as an indication of future performance. All fund performance data is net of management fees. Screening out sectors or companies may result in less diversification and hence more volatility in investment values. The information provided in the marketing material does not constitute, and should not be construed as, investment advice or a recommendation to buy, sell or otherwise transact in the Funds.

Our BMO Sustainable Universal MAP range is really gaining traction. Our Universal MAP concept is simple – to redefine value by offering actively managed multi-asset portfolios at a price more commonly associated with passive investing. We launched our original MAP range in 2017, adding the Sustainable Cautious, Balanced and Growth funds to the line-up in 2019. These have since been joined by Defensive and Adventurous options to complete the five-fund sustainable range. With an OCF capped at 0.39%, these risk-targeted funds are each managed with the defined ‘Avoid, Invest, Improve’ philosophy that underpins all our ESG funds and solutions. As the name suggests, the Sustainable MAP range has a clear emphasis on sustainability – that means the funds focus on companies making a positive contribution to the world we live in. Many of these operate within themes like ‘sustainable mobility’, ‘energy transition’ and ‘health and wellbeing’. With increasing demand from individuals keen to make a positive difference with their investment choices, the funds provide a welcome addition to the advice toolkit.

What solutions are proving popular with advisers?

Responsible investment is becoming an increasingly ‘us too’ marketplace, so it’s key for clients to really consider whether an asset manager’s credentials are what they seem. We think our authenticity sets us apart. Our heritage is a long one and our capabilities are extensive and wide ranging. Perhaps our key differentiator, though, is how responsible considerations are integral to our entire ethos as a business. We’re not an asset manager that just happens to offer some ESG-orientated funds alongside our other products – being responsible about investment sits central to all our activities and processes.

In an increasingly crowded space, what sets BMO apart?

Responsible investment has moved mainstream and the role our industry must play in helping the world respond to major global challenges such as climate change is well recognised. We think this is a great move forwards and are committed to continuing to pioneer action in this space. For our business more specifically, we will continue to consider how we can expand and refine our related product offerings. Our unique experience and breadth of expertise in ESG investing means we are well positioned to continue to develop our offering in this space.

What’s next for you and the wider ESG universe?

For more information on Responsible Investing at BMO and our award-winning ranges, please contact sales.support@bmogam.com or visit bmogam.com/responsibleinvesting

We’ve mentioned becoming a founder signatory of the UN PRI in 2005 and 15 years later the Net Zero Asset Owners Alliance. From an active ownership perspective, we began engaging on climate change in 2000 as a founding theme for our reo® service, started systematically asking companies for climate scenario analysis in 2014 and integrated climate change into voting policies in 2019. In terms of ESG integration, in 2012 we began producing ESG portfolio analytics that included carbon footprint analysis, and in 2016, we published our first impact report that included climate metrics. 2011 saw the launch of the Climate Opportunity Partners Private Equity Fund, and in 2017 we committed to zero fossil fuel reserves across our responsible funds. In 2019, we launched our BMO SDG Engagement Global Equity Fund, in which we engage extensively with companies around SDG 13: Climate Action.

• • • • •

We offer a comprehensive suite of responsible products – each one underpinned by our defined Avoid, Invest, Improve philosophy.

CONTENT BY

This information is for investment professionals only and should not be relied upon by private investors. The value of investments and the income from them can go down as well as up and clients may get back less than they invest. Past performance is not a guide to the future. Investors should note that the views expressed may no longer be current and may have already been acted upon. Changes in currency exchange rates may affect the value of an investment in overseas markets. Investments in emerging markets can be more volatile than other more developed markets. Reference to specific securities should not be interpreted as a recommendation to buy or sell these securities, but is included for the purposes of illustration only. The Fidelity Sustainable Asia Equity Fund has the potential of having high volatility either due to its composition or portfolio management techniques. It can also use financial derivative instruments for investment purposes, which may expose it to a higher degree of risk and can cause investments to experience larger than average price fluctuations. Please note that at least 70% of the portfolio invests in Asia ex-Japan stocks with strong sustainability characteristics - a minimum ESG rating of BB by MSCI. However, the portfolio managers will aim to achieve a higher threshold, targeting at least 70% of the portfolio invested in companies rated BBB and above by MSCI. If unrated by MSCI, rated C or above by Fidelity Sustainability Ratings. Our ratings score issuers on an A-E scale and trajectory forecast based on fundamental bottom-up research and materiality assessment using criteria specific to the industry of each company. A focus on securities of companies which maintain strong environmental, social and governance ("ESG") credentials may result in a return that at times compares unfavourably to similar products without such focus. No representation nor warranty is made with respect to the fairness, accuracy or completeness of such credentials. The status of a security's ESG credentials can change over time. This material was created by Fidelity International. It must not be reproduced or circulated to any other party without prior permission of Fidelity. Investments should be made on the basis of the current prospectus, which is available along with the Key Investor Information Document, current annual and semi-annual reports free of charge on request by calling 0800 368 1732. Fidelity only gives information on products and services and does not give investment advice to retail clients based on individual circumstances. Any comments or statements made are not necessarily those of Fidelity. All e-mails may be monitored. Issued by FIL Pensions Management, authorised and regulated by the Financial Conduct Authority and Financial Administration Services Limited, authorised and regulated by the Financial Conduct Authority. Fidelity International, the Fidelity International logo and F symbol are trademarks of FIL Limited. UKM0321/34008/SSO/NA

Investing strategies focused on environment, social and governance factors, better known as ESG strategies, often employ screening, exclusions, and integration among other tactics. But at their core, all these strategies are about investing in ‘sustainable’ businesses. While simplistic, achieving a long-term future for any business hinges on sustainability pervading all aspects of the company. To be clear: a company that ignores its environmental externalities, is unable to retain talent, or isn’t compliant with regulations won’t be able to sustain its operations into the future. Conversely, as numerous studies have shown, companies with higher sustainability characteristics deliver superior long-term value. Here we clarify the link between sustainability and value creation. There’s general agreement about why this link exists - a business which doesn’t pursue stakeholder value creation or ignores the E, S or G aspects is bound to stumble and destroy value, like a car with one or more wobbly wheels. Here, we aim to address the ‘how’ of assessing this via our valuation approaches.

A recent example is China’s peer-to-peer (P2P) lending industry, which saw rapid growth until a few years ago. By June 2018, estimated P2P outstanding loans topped 1 trillion renminbi ($155 billion). Before regulators stepped in, companies such as Yirendai, Paipaidai and Qudian were charging effective interest rates as high as 35-40%. Since then, regulatory intervention has helped lead to a dismantling of China’s P2P lending industry. Investors looking at the sector’s rapid rise through a sustainability lens might have been better able to sidestep some of the value destruction that ultimately ensued. Interest rates charged by some companies were clearly excessive and unsustainable. The story of Martin Shkreli’s Turing Pharma is another case of an unsustainable business model, whereby the firm in its bid to boost profits, put through massive price increases for life-saving medicines that then became unaffordable for patients. Value destruction can also come from running businesses with unsustainable debt structures such as General Electric, which was recently forced to undertake significant asset sales to pare down debt.

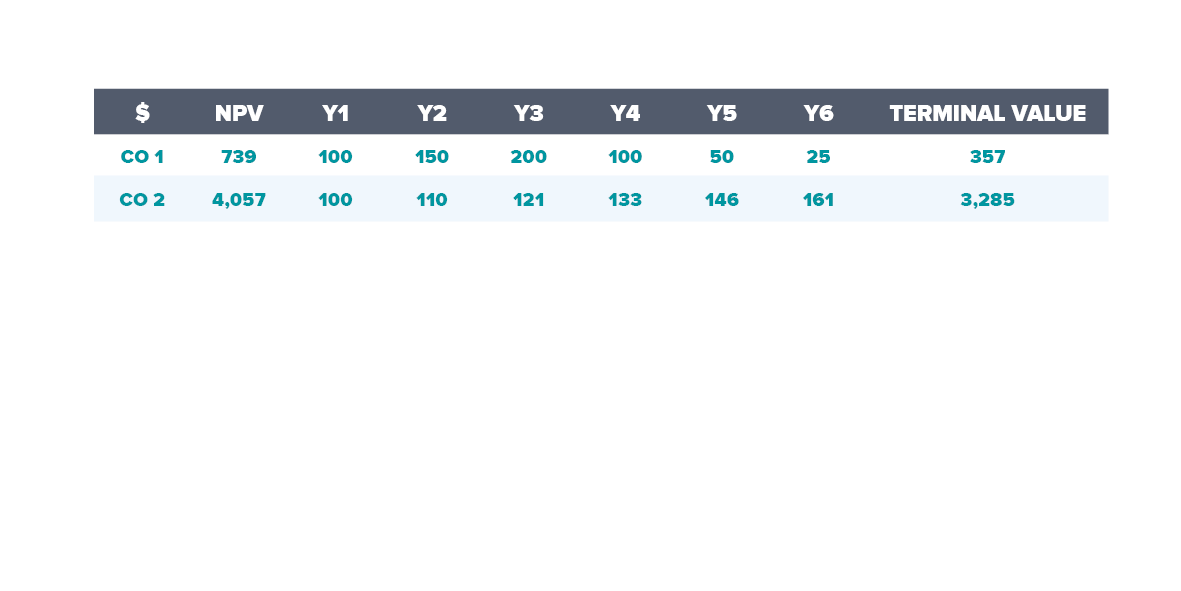

All valuation methodologies, whether traditional ones of price to earnings and price to book, or the recently popular ones like price to sales or enterprise value to sales, are essentially shortcuts to understanding the present value of future cash flows, which investors also calculate via a discounted cash flow (DCF) analysis. In the example below, Company 1 and Company 2 are in the same industry facing similar dynamics. They both generated $100 of free cash flow in Year 1. Company 1 focused on growth and has pushed a new generation product, despite potential safety hazards for its customers. Company 2 focused on product safety and was willing to invest in a higher R&D effort, at the cost of some near-term cash flows. After a few years, Company 1 experiences safety issues that triggers regulatory intervention, leading to a reset in its FCF down to $25 by Year 6. Additionally, there’s now no earnings growth potential for Company 1. Company 2 sees steady growth and gives us the confidence to project a 3% terminal growth for its products. Using a similar 7% discount rate for the two companies, we can see the results:

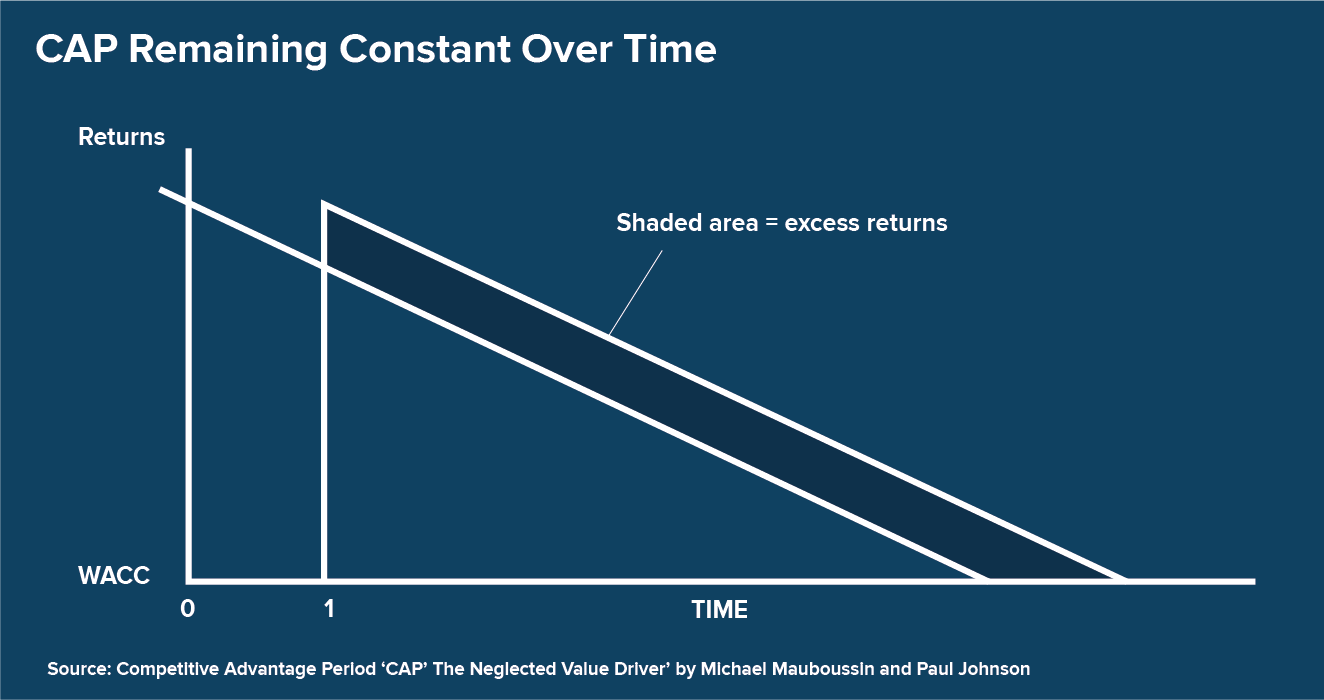

The principle of sustainability is linked to the concept of Competitive Advantage Period (CAP) developed by Miller & Modigliani (1961), which was expanded upon by Michael Mauboussin and Paul Johnson (1997). Essentially, the longer a company can expand its CAP, the more value it creates. Let’s expand this concept further by calling it Sustainable Competitive Advantage Period (SCAP). This is a period during which, by virtue of its ESG and stakeholder-centric business practices, a company can reduce the risks to CAP longevity and prolong this period thereby driving value.

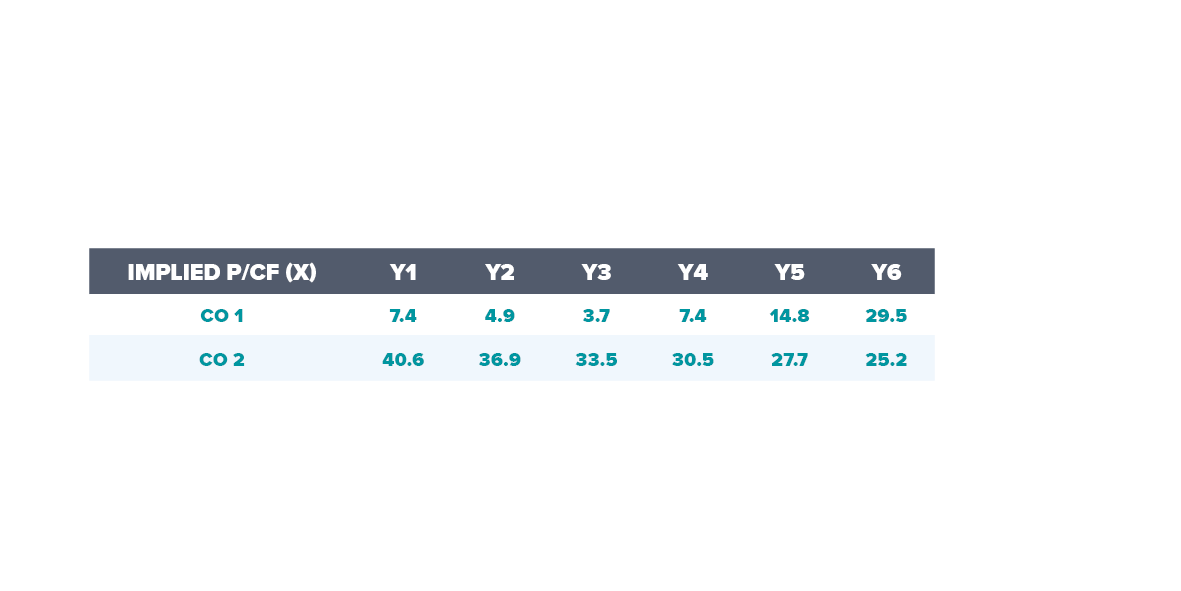

For simplicity, we discounted both companies by the same rate, but this might have been too generous. In reality, Company 1 should see its cash flows discounted by a much higher rate given the inherently higher risk in its business operations. As an alternate example, let’s take a look at another commonly used valuation metric - P/E ratios. This approach considers the earnings power of the business now and awards the company a ‘n’ number of years of realizing such earnings. While ‘n’ depends on a few other variables such as growth, returns and cost of capital, the sustainable period of excess returns is a key driver of the P/E multiple. When we look at P/E (we assume free cash flows are equivalent to earnings to keep it simple) for two companies in the early years of the forecast horizon, the results are stark. Company 1 deserved a much lower multiple to discount for the lack of sustainability in its operations. However, it is very likely that the market would ascribe it a much higher multiple than Company 2 in the early years of strong growth.

That’s what makes sustainability important and key to long-term value creation. It can help close the gap between expectations and outcomes, while protecting an investment from a permanent loss of capital.

Some red flags to observe include excessive returns, complex business structures, lack of regulatory clarity, short-term focused management incentive structures, low or no focus on a stakeholder analysis, and reliance on debt to enhance returns. While not a comprehensive list, viewing any business through a sustainability lens can help investors allocate capital to companies that will drive long-term value creation and mitigate exposure to permanent loss of capital. In the case of the aforementioned Chinese P2P industry, excessive returns of the lenders, complex fee structures and lack of regulatory clarity were all red flags.

Avoiding value destruction through a ‘sustainability’ lens

Valuation implications

What are the red flags?

Sustainability - a key part of investment analysis

Sustainability of a business is a key input in estimating its potential for value creation. While analysts tend to focus on estimating the competitive advantage period, true sustainability comes when a business takes it farther, with a focus on relevant ESG aspects and by adopting a stakeholder-centric approach. A comprehensive evaluation of sustainability should be a key part of any investment analysis.

Inside Fidelity: Sustainable engagement

Register now: 11 May, 8:30-9:30am

Learn about Fidelity’s active engagement

Learn more about the Fidelity Sustainable Asia Equity Fund

Dhananjay Phadnis, Lead Portfolio Manager

by Dhananjay Phadnis, Lead Portfolio Manager and Flora Wang, Co- Portfolio Manager, Fidelity Sustainable Asia Equity Fund

Most investors can agree that environmental, social and governance (ESG) factors help determine a company’s prospects for long-term value creation. But how should we quantify the valuation impact of sustainable investing?

While simplistic, achieving a long-term future for any business hinges on sustainability pervading all aspects of the company

Flora Wang, Co-Portfolio Manager

The value of an investment and the income from it can fall as well as rise as a result of market and currency fluctuations, you may not get back the amount originally invested. Past performance should not be seen as a guide to future performance. If you are unsure which investment is most suited for you, the advice of a qualified financial adviser should be sought. EdenTree Investment Management Limited (EdenTree) Reg. No. 2519319. Registered in England at Benefact House, 2000, Pioneer Avenue, Gloucester Business Park, Brockworth, Gloucester, GL3 4AW, United Kingdom. EdenTree is authorised and regulated by the Financial Conduct Authority and is a member of the Investment Association. Firm Reference Number 527473.

The UK has one of the longest standing histories in respect of responsible and sustainable investing, and the region has been a fruitful source of returns for ESG investors over the long term. The last few years, however, have been difficult for responsible and sustainable investors in UK equities. A combination of negative Brexit sentiment and the coronavirus pandemic have weighed heavily on share prices and hampered investor confidence in the market. Although demand for ESG investing continues to grow more widely, the UK has been largely overlooked and under-allocated to, as other regions have outperformed. Despite this, at EdenTree we remain committed responsible and sustainable investors in UK equities. We believe the UK has a unique opportunity to take a global leadership position as a market for ESG investors, driven by a number of sustained industry trends and a more supportive macro-economic picture for UK equities as we move through 2021.

A key development is the enormous shift in attitude towards ESG issues that we have seen over the last few years, putting the UK government and capital markets on a positive trajectory to embrace responsible and sustainable factors. For example, we now have previously unseen commitments from the UK government to achieving environmental targets. The pandemic has accelerated this trend in a number of ways. Firstly, it has brought social issues into much greater prominence, clearly highlighting the social inequities and injustice that exist within the current global financial and economic system. Secondly, the vast wave of new fiscal stimulus packages to combat the pandemic slowdown in most major developed economies is noticeably targeting green technologies and infrastructure. This was apparent in the UK’s stimulus package, which included plans to quadruple offshore wind power, boost hydrogen production, invest in carbon capture technologies and make London the capital of green finance. Finally, we are seeing strong support from financial institutions and industry bodies to make positive change. For example, Andrew Bailey, the governor of the Bank of England, has spoken out on the important role that capital markets have to play in achieving the transition to a resilient, carbon-neutral economy. This, combined with the supportive macro-economic backdrop – low interest rates and low inflation driven by ongoing monetary and fiscal policy – and hopes of the UK economy re-opening as the vaccine rollout continues, is leading us on an irreversible trend towards an increased responsible and sustainable opportunity set for UK equity investors.

Responsible and sustainable investors in UK equities are now faced with a potentially compelling investment opportunity, provided they are willing to look through the noise and short-term uncertainty. ESG investors must focus on how the UK is positioned for longer-term future growth, combined with the fact that the region provides a rich seam of companies that are ESG leaders, across sectors such as healthcare, industrials, materials and technology, providing us as responsible and sustainable investors with plenty of stock-picking opportunities.

By Ketan Patel and Philip Harris

The pandemic has brought social issues into much greater prominence, clearly highlighting the social inequities and injustices that exist within the current global financial and economic system

Supportive environment for ESG investors

UK equities overlooked

This being the case, fund buyers who want to capitalise on this need an investment manager with a deep expertise of both the UK and the responsible and sustainable investment landscape. EdenTree brought one of the first ethical UK equity funds to market more than 33 years ago, so we are firmly embedded in the fabric of responsible and sustainable investing within the UK. EdenTree’s Responsible & Sustainable UK Equity fund and our Responsible & Sustainable UK Equity Opportunities fund provide investors with a more complete allocation to UK equities as a whole, which should deliver regardless of market environment. At the heart of our approach we are responsible and sustainable, bottom-up stock-pickers who look for quality growth and earnings quality across all the companies we invest in. This ‘quality’ is attributed to companies that are market leaders in their field with defendable market share, attractive profit margins and solid cash flows – growth and returns on capital can only be predicated on these key attributes. The EdenTree Responsible & Sustainable UK Equity fund focuses on investing in companies that are resilient across all types of economic climate, and exhibit strong fundamentals. Looking for these opportunities primarily across the large and mid-cap spectrum, such an approach has proven over the long term to result in significant outperformance and offer more protection through challenging market conditions. The EdenTree Responsible & Sustainable UK Equity Opportunities fund puts growth at the heart of its strategy. The team takes a highly analytical and hands-on approach to stock-picking, aimed at reducing risk and enhancing returns. Key to outperformance and adding alpha is the fund’s focus on the mid and small-cap space. Both funds are also managed in accordance with our responsible and sustainable approach. We fully integrate ESG risk factors across our investment process in order to deliver superior returns and add value for clients. This integrated approach covers four key areas: screening, engagement, governance and thought leadership research, for a truly active responsible and sustainable approach.

EdenTree’s Responsible & sustainable approach

Stars aligning for ESG investors in UK equities

Ketan Patel, fund manager of the EdenTree Responsible & Sustainable UK Equity Fund

Philip Harris, fund manager of the EdenTree Responsible & Sustainable UK Equity Opportunities Fund.